The Commercial Reimbursement Gap: Why Many Health Systems Are Leaving Significant Revenue on the Table

The Commercial Reimbursement Gap Is Larger Than Most Organizations Realize

Most health systems assume their commercial reimbursement rates are reasonably aligned with the market. In many cases, they are not.

In the organizations and markets we analyze, we consistently find meaningful gaps between what a health system is paid and what comparable peers receive for the same services. These gaps are rarely obvious. But they are often material enough to meaningfully impact long-term financial performance.

The challenge is not simply a handful of underperforming contracts or isolated coding categories. In many cases, the issue is systemic. Contract structures that were negotiated years ago may no longer reflect an organization’s market position, specialty mix, service line strength, or strategic value within a region.

Known as the commercial reimbursement gap, it’s the difference between what an organization is currently paid and what the market may support based on peer positioning, service capabilities, and payer dynamics.

For many organizations, that gap is larger than expected.

The Commercial Reimbursement Gap Is Larger Than Most Organizations Realize

In payer strategy engagements, it is not uncommon to identify organizations being reimbursed at materially lower levels than comparable peers for the same services.

In one example, a single commercial payer contract at a 350-bed hospital (its largest) was underperforming median peer reimbursement by an estimated $15 million. In another, an organization that served as the exclusive provider of highly acute inpatient services within a 250-mile radius was still reimbursed in the bottom quartile of its market.

What makes these situations notable is that neither organization believed it had a major reimbursement problem at the outset of the analysis.

In many cases, the issue is not visible from traditional reporting alone. Revenue cycle data may show stable collections and contract performance, while broader market benchmarking reveals significant underpayment relative to peers.

The pattern also tends to repeat across categories:

- inpatient DRGs

- outpatient hospital reimbursement

- physician fee schedules

- high-volume CPT groupings

- specialty and procedural services

More importantly, the gaps are rarely isolated to a few codes. They are often structural.

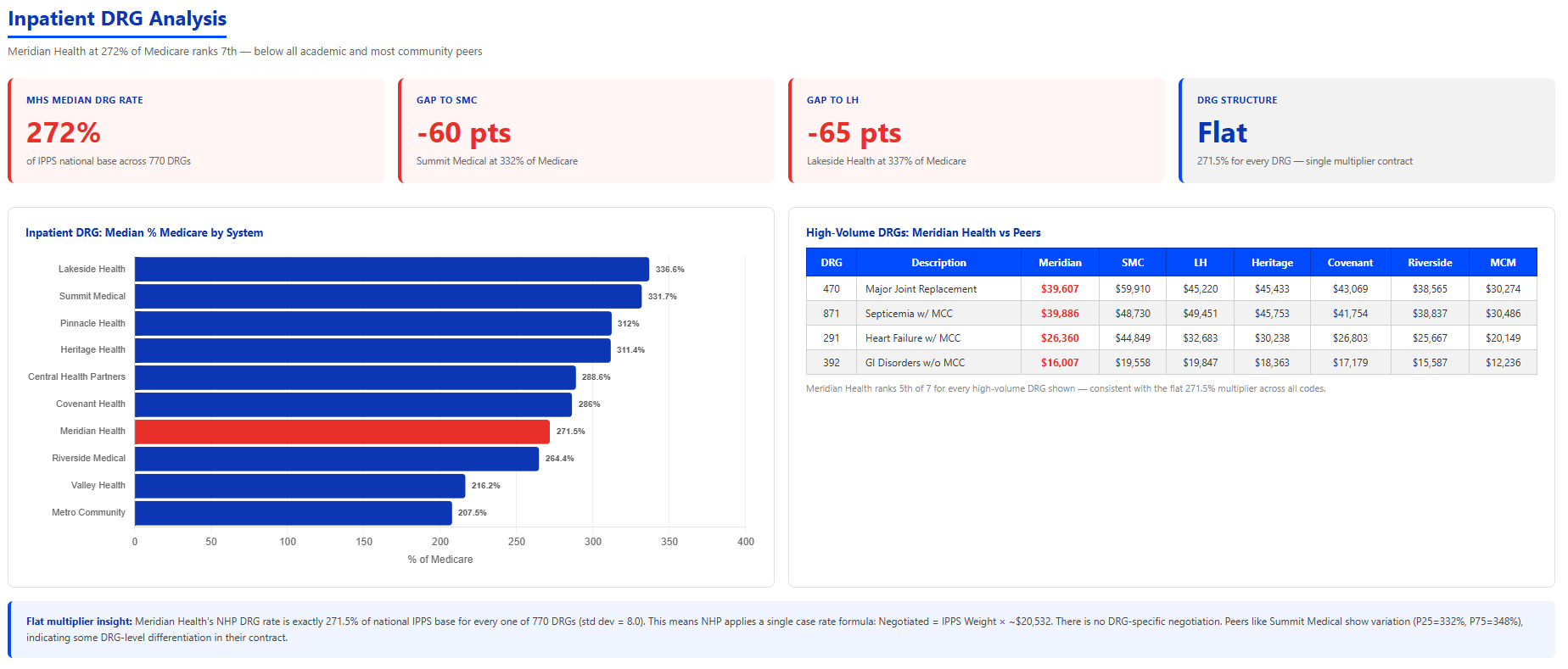

One common example is the use of flat reimbursement structures, where a single multiplier is applied broadly across hundreds of DRGs or service categories regardless of market variation, service complexity, or specialty differentiation. While these arrangements may simplify administration, they can create substantial long-term disadvantage if not periodically reevaluated against the market.

In this case, the organization’s inpatient reimbursement structure applied essentially the same multiplier across more than 700 DRGs. Peer organizations demonstrated significantly greater differentiation across service lines and acuity categories, creating substantial reimbursement separation over time.

The result was not simply a few underperforming codes. It was a contract structure that consistently underperformed relative to the market.

What Leading Organizations Are Doing Differently

Organizations that manage payer strategy most effectively tend to approach reimbursement as an ongoing strategic discipline rather than a reactive contract administration function.

Instead of waiting for negotiations to begin, leading organizations often spend 12-to-18 months building a defensible fact base before contract renewal discussions occur.

That preparation typically includes:

- benchmarking reimbursement against comparable markets and peer cohorts

- identifying service-line-specific opportunities and vulnerabilities

- modeling financial impact across payer scenarios

- establishing target outcomes and fallback thresholds before negotiations begin

Importantly, these organizations are not approaching payer contract negotiations defensively.

They are entering negotiations with a defined market position, a quantified understanding of reimbursement opportunity, and a strategic framework for prioritizing where renegotiation effort can create the greatest impact. That distinction matters.

Organizations operating reactively often negotiate based on payer-provided benchmarks, historical contract assumptions, or generalized market impressions. Organizations operating proactively tend to negotiate from a position supported by market intelligence, scenario modeling, and detailed reimbursement analysis.

The difference between those two approaches can materially affect long-term revenue performance.

Why Many Organizations Still Miss the Problem

The commercial reimbursement gap persists largely because most organizations lack complete visibility into how their contracts compare to the broader market.

Healthcare organizations generate enormous amounts of financial and operational data internally. However, that data is rarely structured in a way that enables meaningful peer reimbursement comparison at the level required for strategic payer analysis.

At the same time, payer contracts have become increasingly complex, layered with carve-outs, escalators, case-rate arrangements, specialty provisions, and custom fee schedule structures that vary by site of care and service line.

Over time, those terms accumulate, creating an environment where true reimbursement positioning becomes difficult to evaluate without a highly detailed benchmarking process.

The issue is compounded by the lack of a universal market benchmark.

Every market behaves differently. Competitive positioning varies by geography, payer mix, academic presence, specialty concentration, referral dynamics, and service line strength. A reimbursement structure that appears competitive in one category may materially underperform in another.

This is why broad national averages or generalized benchmarking summaries often fail to tell the full story.

Meaningful payer strategy requires a more nuanced understanding of:

- market-specific reimbursement patterns

- peer differentiation

- specialty-level positioning

- contract structure dynamics

- service-line economics

- payer behavior within a given region

In many cases, the organizations most at risk are not financially unsophisticated. They operate with incomplete market visibility, while payers maintain a significantly broader view of regional reimbursement dynamics.

Why This Matters More Now

For years, many organizations viewed payer contracting primarily as a maintenance exercise: preserve relationships, secure incremental increases, and avoid disruption.

That environment is changing.

Health systems today are operating under sustained financial pressure while simultaneously facing:

- rising labor costs

- increasing denials and write-offs

- pressure on operating margins

- movement away from traditional percentage-of-charge structures

- growing scrutiny from boards and executive leadership regarding revenue performance

At the same time, reimbursement transparency and market intelligence capabilities are reshaping payer negotiations.

Organizations that proactively establish a clear understanding of their market position may be better positioned to capitalize on future rate rebalancing opportunities. Organizations that delay may find themselves negotiating from a weaker position as payers become increasingly selective about where they concede reimbursement increases.

In other words, there may be a growing first-mover advantage.

Payers are unlikely to allow the pie to expand indefinitely. As reimbursement pressure intensifies, organizations that can clearly demonstrate their market position and strategic value may be better positioned than those that approach negotiations reactively.

This creates the potential for market winners and losers over the next several contract cycles.

Leveling the Playing Field

Most organizations lack a clear view of how their commercial reimbursement compares with peers across service lines, specialties, sites of care, and contract structures.

Without that visibility, payer strategy often remains reactive, responding to payer proposals rather than being grounded in a defensible understanding of market position and reimbursement opportunity.

The organizations navigating this environment most effectively are not simply negotiating harder. They are negotiating with a stronger fact base, clearer market intelligence, and a more disciplined strategic approach. The goal is not simply awareness; instead, it is leveling the playing field.

Organizations that understand whether they are above, at, or below market are better positioned to make informed strategic decisions, prioritize negotiations, and pursue reimbursement structures that more accurately reflect the value they deliver within their markets.

Ready to understand where your organization stands?